Page 19 - Demo

P. 19

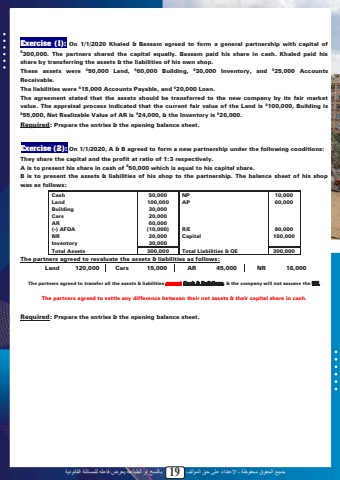

%u062c%u0645%u064a%u0639 %u0627%u0644%u062d%u0642%u0648%u0642 %u0645%u062d%u0641%u0648%u0638%u0629 %u0640 %u0627%u0625%u0644%u0639%u062a%u062f%u0627%u0621 %u0639%u0644%u0649 %u062d%u0642 %u0627%u0644%u0645%u0624%u0644%u0641 19 %u0628%u0627%u0644%u0646%u0633%u062e %u0623%u0648 %u0627%u0644%u0637%u0628%u0627%u0639%u0629 %u064a%u0639%u0631%u0636 %u0641%u0627%u0639%u0644%u0647 %u0644%u0644%u0645%u0633%u0627%u0626%u0644%u0629 %u0627%u0644%u0642%u0627%u0646%u0648%u0646%u064a%u0629Exercise (1): On 1/1/2020 Khaled & Bassam agreed to form a general partnership with capital of $300,000. The partners shared the capital equally. Bassam paid his share in cash. Khaled paid his share by transferring the assets & the liabilities of his own shop.These assets were $50,000 Land, $60,000 Building, $30,000 Inventory, and $25,000 Accounts Receivable.The liabilities were $15,000 Accounts Payable, and $20,000 Loan.The agreement stated that the assets should be transferred to the new company by its fair market value. The appraisal process indicated that the current fair value of the Land is $100,000, Building is $55,000, Net Realizable Value of AR is $24,000, & the Inventory is $26,000. Required: Prepare the entries & the opening balance sheet.Exercise (2): On 1/1/2020, A & B agreed to form a new partnership under the following conditions:They share the capital and the profit at ratio of 1:3 respectively.A is to present his share in cash of $50,000 which is equal to his capital share.B is to present the assets & liabilities of his shop to the partnership. The balance sheet of his shop was as follows:Cash 50,000 NP 10,000Land 100,000 AP 60,000Building 30,000Cars 20,000AR 60,000(-) AFDA (10,000) R/E 80,000NR 20,000 Capital 150,000Inventory 30,000Total Assets 300,000 Total Liabilities & OE 300,000The partners agreed to revaluate the assets & liabilities as follows:Land 120,000 Cars 15,000 AR 45,000 NR 18,000The partners agreed to transfer all the assets & liabilities except Cash & Buildings, & the company will not assume the NP.The partners agreed to settle any difference between their net assets & their capital share in cash.Required: Prepare the entries & the opening balance sheet.17