Page 41 - Demo

P. 41

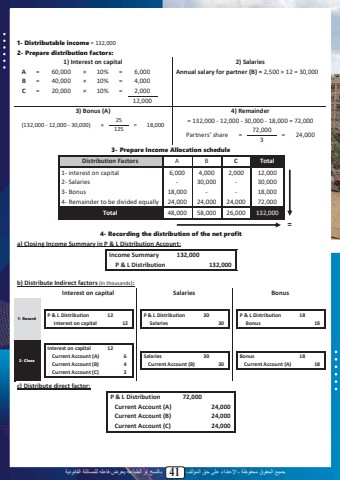

%u062c%u0645%u064a%u0639 %u0627%u0644%u062d%u0642%u0648%u0642 %u0645%u062d%u0641%u0648%u0638%u0629 %u0640 %u0627%u0625%u0644%u0639%u062a%u062f%u0627%u0621 %u0639%u0644%u0649 %u062d%u0642 %u0627%u0644%u0645%u0624%u0644%u0641 41 %u0628%u0627%u0644%u0646%u0633%u062e %u0623%u0648 %u0627%u0644%u0637%u0628%u0627%u0639%u0629 %u064a%u0639%u0631%u0636 %u0641%u0627%u0639%u0644%u0647 %u0644%u0644%u0645%u0633%u0627%u0626%u0644%u0629 %u0627%u0644%u0642%u0627%u0646%u0648%u0646%u064a%u06291- Distributable income = 132,0002- Prepare distribution factors:1) Interest on capital 2) SalariesA = 60,000 %u00d7 10% = 6,000B = 40,000 %u00d7 10% = 4,000C = 20,000 %u00d7 10% = 2,00012,000Annual salary for partner (B) = 2,500 %u00d7 12 = 30,0003) Bonus (A) 4) Remainder(132,000 - 12,000 - 30,000) %u00d7 25 = 18,000 125= 132,000 - 12,000 - 30,000 - 18,000 = 72,000Partners%u2019 share = 72,000 = 24,000 33- Prepare Income Allocation scheduleDistribution Factors A B C Total1- interest on capital 6,000 4,000 2,000 12,0002- Salaries - 30,000 - 30,0003- Bonus 18,000 - - 18,0004- Remainder to be divided equally 24,000 24,000 24,000 72,000Total 48,000 58,000 26,000 132,0004- Recording the distribution of the net profita) Closing Income Summary in P & L Distribution Account:Income Summary 132,000P & L Distribution 132,000b) Distribute Indirect factors (in thousands):Interest on capital Salaries Bonus1- RecordP & L Distribution 12Interest on capital 12P & L Distribution 30Salaries 30P & L Distribution 18Bonus 182- CloseInterest on capital 12Current Account (A) 6Current Account (B) 4Current Account (C) 2Salaries 30Current Account (B) 30Bonus 18Current Account (A) 18c) Distribute direct factor:P & L Distribution 72,000Current Account (A) 24,000Current Account (B) 24,000Current Account (C) 24,000=39