Page 69 - Demo

P. 69

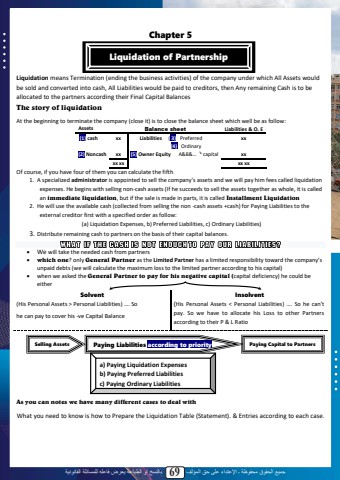

%u062c%u0645%u064a%u0639 %u0627%u0644%u062d%u0642%u0648%u0642 %u0645%u062d%u0641%u0648%u0638%u0629 %u0640 %u0627%u0625%u0644%u0639%u062a%u062f%u0627%u0621 %u0639%u0644%u0649 %u062d%u0642 %u0627%u0644%u0645%u0624%u0644%u0641 69 %u0628%u0627%u0644%u0646%u0633%u062e %u0623%u0648 %u0627%u0644%u0637%u0628%u0627%u0639%u0629 %u064a%u0639%u0631%u0636 %u0641%u0627%u0639%u0644%u0647 %u0644%u0644%u0645%u0633%u0627%u0626%u0644%u0629 %u0627%u0644%u0642%u0627%u0646%u0648%u0646%u064a%u0629Chapter 5Liquidation means Termination (ending the business activities) of the company under which All Assets would be sold and converted into cash, All Liabilities would be paid to creditors, then Any remaining Cash is to be allocated to the partners according their Final Capital BalancesThe story of liquidationAt the beginning to terminate the company (close it) is to close the balance sheet which well be as folloAssets Balance sheet Liabilities & O. E(1) cash xx Liabilities ( 3) Preferred (4) Ordinaryxx(2) Noncash xx (5) Owner Equity A&B&%u2026 %u2019s capital xxxx xx xx xxOf course, if you have four of them you can calculate the fifth1. A specialized administrator is appointed to sell the company's assets and we will pay him fees called liquidation expenses. He begins with selling non-cash assets (If he succeeds to sell the assets together as whole, it is called an immediate liquidation, but if the sale is made in parts, it is called Installment Liquidation2. He will use the available cash (collected from selling the non -cash assets +cash) for Paying Liabilities to the external creditor first with a specified order as follo(a) Liquidation Expenses, b) Preferred Liabilities, c) Ordinary Liabilities)3. Distribute remaining cash to partners on the basis of their capital balances.%u2022 We will take the needed cash from partners %u2022 which one? only General Partner as the Limited Partner has a limited responsibility toward the company%u2019s unpaid debts (we will calculate the maximum loss to the limited partner according to his capital) %u2022 when we asked the General Partner to pay for his negative capital (capital deficiency) he could be either Solvent Insolvent(His Personal Assets > Personal Liabilities) %u2026. So he can pay to cover his -ve Capital Balance(His Personal Assets < Personal Liabilities) %u2026. So he can't pay. So we have to allocate his Loss to other Partners according to their P & L RatioAs you can notes we have many different cases to deal with What you need to know is how to Prepare the Liquidation Table (Statement). & Entries according to each case.67Liquidation of PartnershipSelling Assets Paying Liabilities according to priority Paying Capital to Partnersa) Paying Liquidation Expenses b) Paying Preferred Liabilitiesc) Paying Ordinary Liabilities