Page 9 - Demo

P. 9

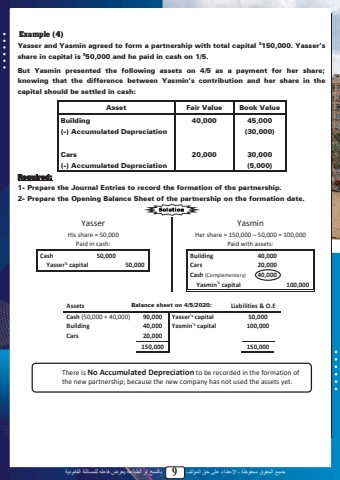

%u062c%u0645%u064a%u0639 %u0627%u0644%u062d%u0642%u0648%u0642 %u0645%u062d%u0641%u0648%u0638%u0629 %u0640 %u0627%u0625%u0644%u0639%u062a%u062f%u0627%u0621 %u0639%u0644%u0649 %u062d%u0642 %u0627%u0644%u0645%u0624%u0644%u0641 9 %u0628%u0627%u0644%u0646%u0633%u062e %u0623%u0648 %u0627%u0644%u0637%u0628%u0627%u0639%u0629 %u064a%u0639%u0631%u0636 %u0641%u0627%u0639%u0644%u0647 %u0644%u0644%u0645%u0633%u0627%u0626%u0644%u0629 %u0627%u0644%u0642%u0627%u0646%u0648%u0646%u064a%u0629Example (4)Yasser and Yasmin agreed to form a partnership with total capital $150,000. Yasser%u2019sshare in capital is $50,000 and he paid in cash on 1/5.But Yasmin presented the following assets on 4/5 as a payment for her share; knowing that the difference between Yasmin%u2019s contribution and her share in the capital should be settled in cash:Asset Fair Value Book ValueBuilding 40,000 45,000(-) Accumulated Depreciation (30,000)Cars 20,000 30,000(-) Accumulated Depreciation (5,000)Required: 1- Prepare the Journal Entries to record the formation of the partnership.2- Prepare the Opening Balance Sheet of the partnership on the formation date.Yasser YasminHis share = 50,000Paid in cash:Cash 50,000Yasser%u2019s capital 50,000Her share = 150,000 %u2013 50,000 = 100,000Paid with assets:Building 40,000Cars 20,000Cash (Complementary) 40,000Yasmin%u2019s capital 100,000Assets Balance sheet on 4/5/2020: Liabilities & O.ECash (50,000 + 40,000) 90,000 Yasser%u2019s capital 50,000Building 40,000 Yasmin%u2019s capital 100,000Cars 20,000150,000 150,0007There is No Accumulated Depreciation to be recorded in the formation of the new partnership; because the new company has not used the assets yet.