Page 87 - Demo

P. 87

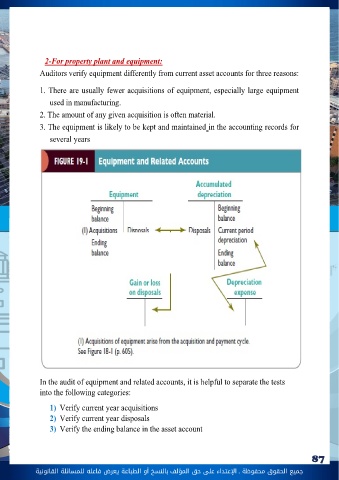

جميع الحقوق محفوظة ـ اإلعتداء عىل حق املؤلف 87 بالنسخ أو الطباعة يعرض فاعله للمسائلة القانونية6- Posting and summarization: all purchases on account transactions recorded A/P master file Third: Design test of Details for accounting Accounts payable, Property plant and equipment1-For A/PWe will use the same balance-related audit objectives to be applied to verifying accounts receivable, as they also apply to liabilities, with three minor modifications: The objectives of auditing the AP balance are: 1. Existence: Recorded accounts Payable exist. o Confirmation of accounts payable o Tracing from accounts payable list to vendors invoice (backward) 2. Completeness: all Existing accounts payable are included.o Trace the receiving documents to the journal entries and subsidiary ledger. (Forward tracing) 3. Accuracy: Accounts payables are accurateo Confirmation of accounts payable balances selected from trial balance is the most common test of detail for accuracy. o Examination of A/P paid before year end and that due after year end by verifying with receiving report and vendors invoice 4. Classification: Accounts payable are correctly classified o Auditor must make sure the client correctly classified AP as Current or long term o Review master file for interest bearing liabilities5. Cutoff: Cutoff for accounts Payable is correcto Cutoff misstatements occur when current period transactions are recorded in the subsequent periods and vice versa