Page 19 - Demo

P. 19

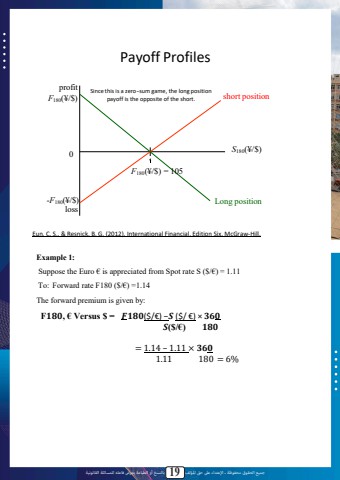

%u062c%u0645%u064a%u0639 %u0627%u0644%u062d%u0642%u0648%u0642 %u0645%u062d%u0641%u0648%u0638%u0629 %u0640 %u0627%u0625%u0644%u0639%u062a%u062f%u0627%u0621 %u0639%u0649%u0644 %u062d%u0642 %u0627%u0645%u0644%u0624%u0644%u0641 19 %u0628%u0627%u0644%u0646%u0633%u062e %u0623%u0648 %u0627%u0644%u0637%u0628%u0627%u0639%u0629 %u064a%u0639%u0631%u0636 %u0641%u0627%u0639%u0644%u0647 %u0644%u0644%u0645%u0633%u0627%u0626%u0644%u0629 %u0627%u0644%u0642%u0627%u0646%u0648%u0646%u064a%u0629Payoff ProfilesprofitF180(%u00a5/$)Since this is a zero%u2212sum game, the long position payoff is the opposite of the short. short position0F180(%u00a5/$) = 105S180(%u00a5/$)-F180(%u00a5/$)lossLong positionEun, C. S., & Resnick, B. G. (2012). International Financial, Edition Six, McGraw-Hill.Example 1:Suppose the Euro %u20ac is appreciated from Spot rate S ($/%u20ac) = 1.11 To: Forward rate F180 ($/%u20ac) =1.14The forward premium is given by:F%ud835%udfcf%ud835%udfcf%ud835%udfd6%ud835%udfd6%ud835%udfce%ud835%udfce, %u20ac Versus $ = %ud835%udc6d%ud835%udc6d%ud835%udfcf%ud835%udfcf%ud835%udfd6%ud835%udfd6%ud835%udfce%ud835%udfce($/%u20ac) %u2212%ud835%udc7a%ud835%udc7a ($/ %u20ac) %u00d7 %ud835%udfd1%ud835%udfd1%ud835%udfd4%ud835%udfd4%ud835%udfce%ud835%udfce%ud835%udc7a%ud835%udc7a($/%u20ac) %ud835%udfcf%ud835%udfcf%ud835%udfd6%ud835%udfd6%ud835%udfce%ud835%udfce= 1.14 %u2013 1.11 %u00d7 %ud835%udfd1%ud835%udfd1%ud835%udfd4%ud835%udfd4%ud835%udfce%ud835%udfce1.11 180 = 6%