Page 121 - Demo

P. 121

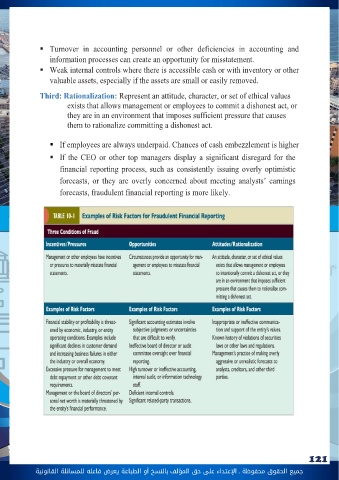

جميع الحقوق محفوظة ـ اإلعتداء عىل حق املؤلف 121 بالنسخ أو الطباعة يعرض فاعله للمسائلة القانونيةThere are Three Basic conditions for fraud that must co-exist for fraud to happen these three conditions are referred to as the Fraud triangleFirst: Incentives: represent the pressure facing Management or other employees to commit fraud: Incentive of misappropriation of assets fraud; Employees with excessive financial obligations, or those with drug abuse or gambling problems, may steal to meet their personal needs. In other cases, dissatisfied employees may steal from a sense of entitlement or as a form of attack against their employers. Incentive of fraudulent financial statements is a decline in the company’s financial prospects. For example, a decline in earnings may threaten the company’s ability to obtain financing. Companies may also manipulate earnings to meet analysts’ forecasts or benchmarks such as prior year earnings, to meet debt covenant restrictions, to achieve a bonus target based on earningsSecond Opportunities: Represent the Circumstances that provide opportunities for management or employees to commit fraud. And are greater in companies in industries where: significant judgments and estimates are involved. For example, valuation of inventories is subject to greater risk of misstatement for companies with diverse inventories in many locations. The risk of misstatement of inventories is further increased if those inventories are at risk for obsolescence.Fourth: Conditions for fraud to happen & Fraud Triangle