Page 14 - Demo

P. 14

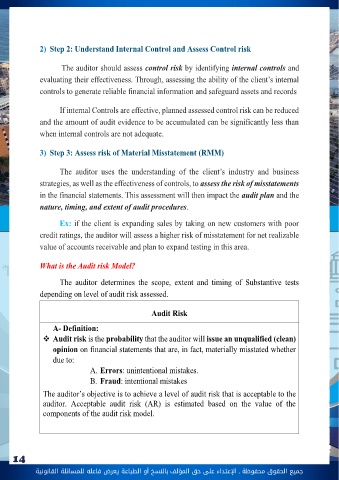

جميع الحقوق محفوظة ـ اإلعتداء عىل حق املؤلف 14 بالنسخ أو الطباعة يعرض فاعله للمسائلة القانونيةPHASE 1: Accepting the client , depends on 4 where the auditor should ( 4 steps) :1) Step 1: Auditors should evaluate new or existing client entity before accepting the audit engagement.To help audit firms identify potential problem clients in advance, any limitation that will be imposed on the auditor before accepting the engagement 2) Step 2: The auditor should Identify the reasons why the client needs to be audited,Whether the client needs to be audited as regulatory requirement as the case of listed firms, to apply for a bank loan or to provide more information to interested users. As it effects his planning of the audit in term of time and efforts assigned to it 3) Step 3: Assigning the appropriate staff:The auditor must make sure he has the required qualification and skills to perform the audit and skilled staff available in time to perform the audit on the agreed upon date. 4) Step 4: Agree to the Fees assignedThe auditor should negotiate and accept the fees assigned to the audit process before accepting the audit engagement. PHASE 2: Planning audit approach Using audit risk Model (three steps):1) Step 1: Obtain an Understanding of the entity and Its environmentThe auditor must have a full understanding of the client’s business and related environment, including knowledge of strategies and processes of his client and it`s industry. The auditor must also understand any unique accounting requirements of the client’s industry.Ex: when auditing an insurance company, the auditor must understand how loss reserves are calculated.