Page 40 - Demo

P. 40

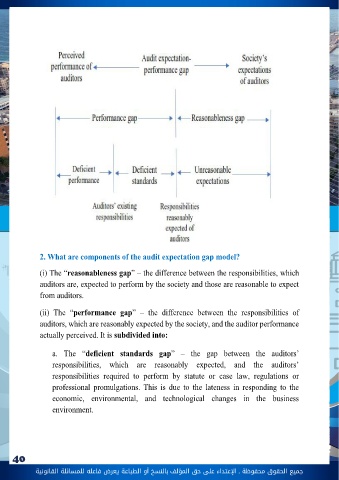

جميع الحقوق محفوظة ـ اإلعتداء عىل حق املؤلف 40 بالنسخ أو الطباعة يعرض فاعله للمسائلة القانونيةSecond: The Audit Expectation Gap Concept, Components and Reasons1) increasing Digital Crimes and Security and Privacy Issues of clients’ Data 2) The increased chances of committing electronic fraud and further chances of discovery by auditors because of each of the following: complexity of electronic operating systems, and applications used the possibility of unauthorized access to data and basic files, the reduction in the time and cost required to commit it, and the difficulty of discovering it as a result of the geographical separation of the audit client workers.1. What is meant by Expectation gap in auditing?It is the difference in opinion between the public and the auditors regarding audit responsibility. Is a gap may exist between what the public expects or needs from auditors and audit profession and what auditors and audit profession can really provide The difference between the expectations of financial statements’ users regarding what the auditor can provide and what is actually provided by him through his audit report VS . The audit responsibilities actually provided by auditors The audit responsibilities expected from society