Page 91 - Demo

P. 91

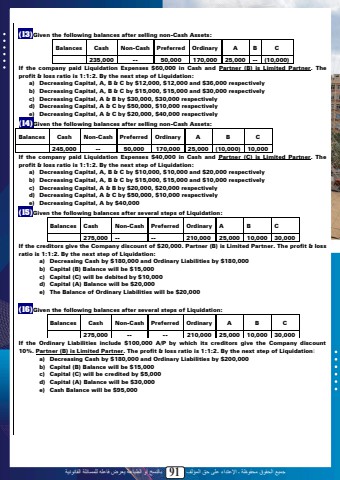

%u062c%u0645%u064a%u0639 %u0627%u0644%u062d%u0642%u0648%u0642 %u0645%u062d%u0641%u0648%u0638%u0629 %u0640 %u0627%u0625%u0644%u0639%u062a%u062f%u0627%u0621 %u0639%u0644%u0649 %u062d%u0642 %u0627%u0644%u0645%u0624%u0644%u0641 91 %u0628%u0627%u0644%u0646%u0633%u062e %u0623%u0648 %u0627%u0644%u0637%u0628%u0627%u0639%u0629 %u064a%u0639%u0631%u0636 %u0641%u0627%u0639%u0644%u0647 %u0644%u0644%u0645%u0633%u0627%u0626%u0644%u0629 %u0627%u0644%u0642%u0627%u0646%u0648%u0646%u064a%u0629(13)Given the following balances after selling non-Cash Assets:Balances Cash Non-Cash Preferred Ordinary A B C235,000 -- 50,000 170,000 25,000 -- (10,000)If the company paid Liquidation Expenses $60,000 in Cash and Partner (B) is Limited Partner. The profit & loss ratio is 1:1:2. By the next step of Liquidation:a) Decreasing Capital, A, B & C by $12,000, $12,000 and $36,000 respectivelyb) Decreasing Capital, A, B & C by $15,000, $15,000 and $30,000 respectivelyc) Decreasing Capital, A & B by $30,000, $30,000 respectivelyd) Decreasing Capital, A & C by $50,000, $10,000 respectivelye) Decreasing Capital, A & C by $20,000, $40,000 respectively(14)Given the following balances after selling non-Cash Assets:Balances Cash Non-Cash Preferred Ordinary A B C245,000 -- 50,000 170,000 25,000 (10,000) 10,000If the company paid Liquidation Expenses $40,000 in Cash and Partner (C) is Limited Partner. The profit & loss ratio is 1:1:2. By the next step of Liquidation:a) Decreasing Capital, A, B & C by $10,000, $10,000 and $20,000 respectivelyb) Decreasing Capital, A, B & C by $15,000, $15,000 and $10,000 respectivelyc) Decreasing Capital, A & B by $20,000, $20,000 respectivelyd) Decreasing Capital, A & C by $50,000, $10,000 respectivelye) Decreasing Capital, A by $40,000(15)Given the following balances after several steps of Liquidation:Balances Cash Non-Cash Preferred Ordinary A B C275,000 -- -- 210,000 25,000 10,000 30,000If the creditors give the Company discount of $20,000. Partner (B) is Limited Partner. The profit & loss ratio is 1:1:2. By the next step of Liquidation:a) Decreasing Cash by $180,000 and Ordinary Liabilities by $180,000b) Capital (B) Balance will be $15,000c) Capital (C) will be debited by $10,000d) Capital (A) Balance will be $20,000e) The Balance of Ordinary Liabilities will be $20,000(16)Given the following balances after several steps of Liquidation:Balances Cash Non-Cash Preferred Ordinary A B C275,000 -- -- 210,000 25,000 10,000 30,000If the Ordinary Liabilities include $100,000 A/P by which its creditors give the Company discount 10%. Partner (B) is Limited Partner. The profit & loss ratio is 1:1:2. By the next step of Liquidation:a) Decreasing Cash by $180,000 and Ordinary Liabilities by $200,000b) Capital (B) Balance will be $15,000c) Capital (C) will be credited by $5,000d) Capital (A) Balance will be $30,000e) Cash Balance will be $95,00089