Page 71 - Demo

P. 71

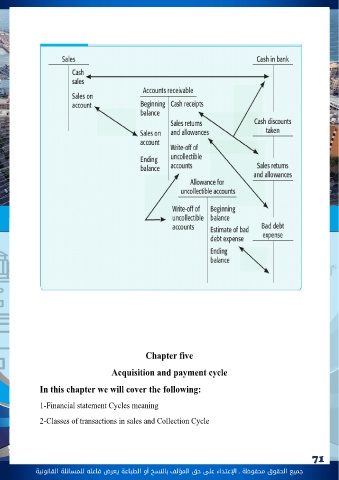

جميع الحقوق محفوظة ـ اإلعتداء عىل حق املؤلف 71 بالنسخ أو الطباعة يعرض فاعله للمسائلة القانونيةo timing difference due to shipments and payments in transit at year end, may require additional investigation, such as inspection of supporting documents. 6) Right and obligations: The client has rights to accounts receivableo Auditors can review clients’ rights to A/R using confirmations o If A portion of A/R used was Pledged as collateral, or sold at discount. The confirmation of receivables will not be enough. So, auditor may review meetings minutes, confirm with banks and examine debt contracts foe evidences of pledged A/R as collaterals 7) Realizable value: Accounts receivable is stated at realizable value (Net realizable valueo Realizable value of A/R (NRV = A/R – AFDA) o AFDA is reasonable. 8) Detail tie-in: Accounts receivable in the aged trial balance agree with related master file amounts, and the total is correctly added and agrees with the general ledger o A/R in subsidiary ledger is correctly added and agrees with the general ledger