Page 74 - Demo

P. 74

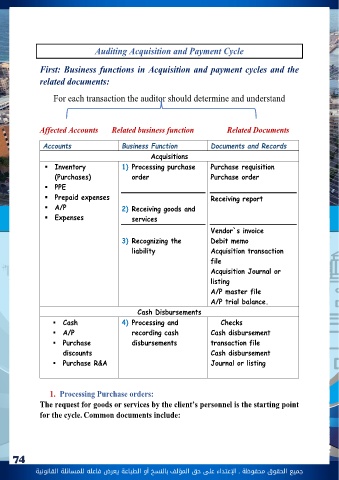

جميع الحقوق محفوظة ـ اإلعتداء عىل حق املؤلف 74 بالنسخ أو الطباعة يعرض فاعله للمسائلة القانونيةFinancial statements Cycleclasses of transactions in Acquisition and Payment CycleFirst: Business functions in Acquisition and Payment Cycle and the related documents:Second: Designing tests of controls and substantive tests of transactions for AcquisitionsThird: Design test of Details for accounting Payable and property plant and equipment BalancesAudits are performed by dividing financial statements into smaller segments or components. The division makes the audit more manageable and aids in the assignments of tasks to different members of the audit team. A company way to divide an audit is to keep closely related types of transactions and account balances in the same segment. This is called the cycle approach. Ex: Purchases, Purchases R& A, Purchase discounts, expenses and acquisition of assets, are classes of transactions that causes accounts payable to increase or decrease. Therefore, they are all parts of Acquisition and Payment Cycle The objective in the audit of the acquisition and payment cycle is to evaluate whether the accounts affected by the acquisitions of goods and services and the cash disbursements for those acquisitions are fairly presented in accordance with accounting standards.