Page 78 - Demo

P. 78

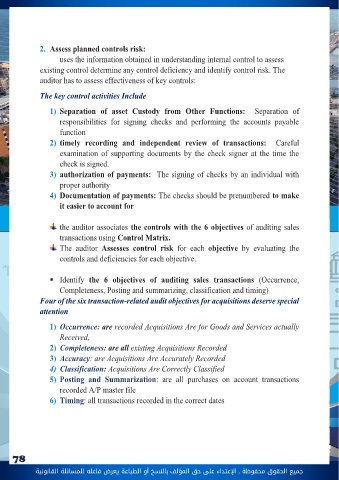

جميع الحقوق محفوظة ـ اإلعتداء عىل حق املؤلف 78 بالنسخ أو الطباعة يعرض فاعله للمسائلة القانونيةc) voucher: containing documents and a package of relevant documents such as the purchase order, copy of the packing slip, receiving report, and vendor’s invoice d) Acquisitions Transaction File This is a computer-generated file that includes all acquisition transactions processed by the accounting system for a period, such as a day, week, or month. It contains all information entered into the system and includes information for each transaction, such as vendor name, date, amount, account classifications, and description and quantity of goods and services purchased. The file can also include purchase returns and allowances or there can be a separate file for those transactions.e) Acquisitions Journal or Listing: often referred to as the purchases journal, is generated from the acquisition’s transaction file The journal or listing includes totals of every account number included for the time period. The same transactions included in the journal or listing are also posted simultaneously to the general ledger and, if they are on account, to the accounts payable master file.f) Accounts Payable Master File: records acquisitions cash disbursements, and acquisition returns and allowances transactions for each vendor.g) Accounts Payable Trial Balance: listing includes the total amount owed to each vendor or for each invoice or voucher at a point in time. It is prepared directly from the accounts payable master file.4. Processing and Recording Cash DisbursementsThe payment for goods and services represents a significant activity for all entities. This activity directly reduces balances in liability accounts, particularly accounts payable. Documents associated with the disbursement process that auditors examine include: