Page 94 - Demo

P. 94

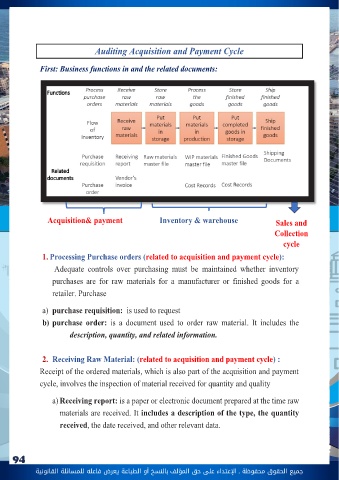

جميع الحقوق محفوظة ـ اإلعتداء عىل حق املؤلف 94 بالنسخ أو الطباعة يعرض فاعله للمسائلة القانونيةFinancial statements Cycle:Chapter six Inventory and warehouse cycle In this Chapter we will cover: 1-Financial statement Cycles meaning 2-Classes of transactions in sales and Collection Cycle 3-Auditing Acquisition and Payment Cycle First: Business functions in Inventory and warehouse cycle and the related documents:Second: Designing tests of controls and substantive tests of transactions for Cost of inventoryThird: Design test of Details for accounting balancesAudits are performed by dividing financial statements into smaller segments or components. The division makes the audit more manageable and aids in the assignments of tasks to different members of the audit team. A company way to divide an audit is to keep closely related types of transactions and account balances in the same segment. This is called the cycle approach. Ex: Inventory, purchases, Raw materials, work in process, Finished goods, Cost of goods sold Therefore they are all parts of Inventory and warehouse cycle. One of the most complex audit accounts, .Factors affecting the complexity of the audit of inventory include 1. Inventory is often the largest account on the balance sheet. 2. Inventory is often in different locations, making physical control and counting difficult. 3. Diverse inventory items such as jewels, chemicals, and electronic parts are often difficult for auditors to observe and value. 4. Inventory valuation is also difficult when estimation of inventory obsolescence is necessary and when manufacturing costs must be allocated to inventory.