Page 98 - Demo

P. 98

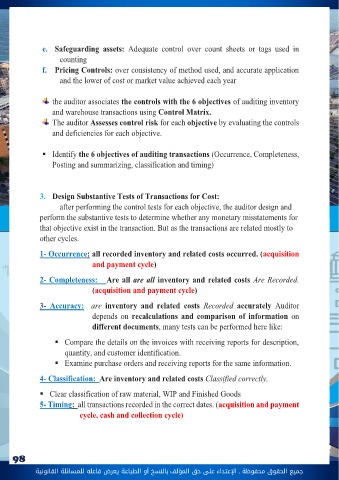

جميع الحقوق محفوظة ـ اإلعتداء عىل حق املؤلف 98 بالنسخ أو الطباعة يعرض فاعله للمسائلة القانونية6. Ship Finished Goods (related to Saled and Collection cycle)Shipping completed goods is part of the sales and collection cycle. The actual shipment of goods to customers in exchange for cash or other assets, c) Shipping documents The function 3, 4, 5: store raw material, process, Store finished goods are the essence of inventory and warehouse cycle and require the auditor to perform additional activities and audit procedures Physically Observe InventoryPrice and Compile InventoryAuditors must observe the client taking a physical inventory count to determine whether recorded inventory actually exists at the balance sheet date and is correctly counted by the client.Physical examination is an essential type of evidence used to verify the existence and count of inventoryCosts used to value inventory must be tested to determine whether the client hascorrectly followed an inventory method that is both in accordance with accountingstandards and consistent with previous years.Examples of key considerations that auditors should consider include the inventory valuation method selected by management, the potential for inventory obsolescence, and the risk that consignment inventory might be intermingled with owned inventory.Must consider consistency of method used, in calculating cost of purchased and manufactured inventory. Whether FIFO of W.A, and accurate application and the. ensure proper valuation of lower of cost or market. also allocating costs of overheads make sure properallocations are assigned.Inventory Observation Requirements:1. Be present at the time the client counts their inventory for determining year-end balanceAssume that the client values an inventory item at $12.00 per unit for 1,000 units, using FIFO. When the auditor examines the most recent invoices for acquisitions of that inventory item, she finds that the most recent acquisition of the inventory item in the year being audited was for 700